In my previous blog, All That Glitters Is Not Gold, I looked at the benefits and issues of long term investments in other precious metal commodities, namely, silver and platinum. The benefits of diversification were noticeable. The platinum futures market, however, is not sufficiently large to make it accessible to investors in any meaningful manner. We found on the basis of the omega measure that the Dow Jones UBS Precious Metals Index fared somewhat better than our equal weighted portfolio of gold and silver in two time periods and worst in the other two time periods. In this blog we will see what happens when you combine precious metals with financial assets using the equally weighted portfolio.

We maintain consistency with the previous blogs by using the same four, five-year time periods of 1991 to 1995, 1996 to 2000, 2001 to 2005 and 2006 to 2010. The financial assets are large capitalization stocks, small capitalization stocks, long term government bonds, intermediate term government bonds and long term corporate bonds as computed by Ibbotson and Associates. Tables 1 to 4 contain monthly return statistics for the five asset classes, precious metals and gold futures. Gold futures were contrasted to financial assets in the blog Asset Allocation and Gold. The statistics are mean, volatility (i.e. standard deviation of returns), minimum, maximum, downside probability, downside loss downside volatility, upside probability, upside reward, upside volatility and omega measure. The upside and downside statistics are partial moments which are introduced in the blog Partial Moments – the Up and Down of Performance and Risk. Omega measure is the ratio of upside reward to downside loss.

On the basis of omega measure, most financial assets outperform precious metals and gold futures. The exception is 2006 to 2010. One has to ask if it pays to combine these commodities with financial assets. Tables 5 and 6 provide a partial answer. Table 5 presents the correlation of precious metals and financial assets while Table 6 highlights the correlations of gold with financial assets. Generally speaking, both gold and precious metals have weak positive or negative correlations with financial assets. Precious metals, as a portfolio, tend to have even more negative or weaker positive correlations. This provides an opportunity to further diversify risk.

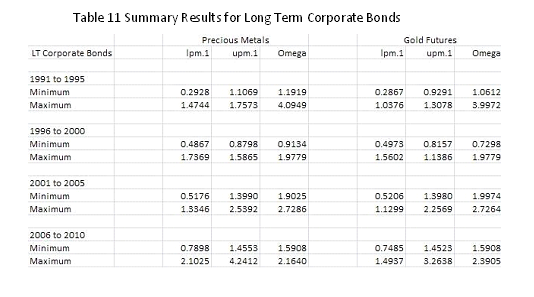

In Asset Allocation and Gold we presented omega frontier charts that show the effect of different mixes of gold and financial assets on the omega measure. These charts are not used here as they tend to have the same appearance and do not reveal information on impact of using precious metals instead of gold as a diversifying investment. Instead, we introduce a new style of analysis in Tables 7 to 11. Each table corresponds to a different financial asset. The time periods are groups of rows with Minimum and Maximum values. There are two groups of columns, one for Precious Metals and the other for Gold Futures. Each group consists of lpm.1 (downside loss), upm.1 (upside reward) and omega. Each value is associated with a portfolio of financial asset and the commodity (gold futures or precious metals). For example, the minimum and maximum upside reward for large cap stocks in Table 7 and for the time period 1991 to 1995 are 1.2799 and 1.9617 for precious metals and 0.9796 and 1.9617 for gold futures. The minimum values are the worst case outcomes for upside reward and the maximum values are the best case outcomes. Notice that precious metals had the greatest worst case outcome when compared to gold whereas both choices had the same best case outcome. In this case, an investor would prefer precious metals as a diversifying investment combined with large capitalization stocks.

If you look at best and worst case outcomes for downside loss, you would probably not want to consider blending silver with gold. The minimum values for downside loss are associated with the minimum loss portfolio as we discussed in the blog Managing Downside Loss with Gold. On the other hand, if you look at the omega measure, a risk adjusted measure of performance; the blend is clearly the best choice for almost all asset classes and time periods. I think that most investors would rather err on the side of more diversification rather than less when dabbling in commodities.

Click to Enlarge

Sponsored by: EMA Softech

No comments:

Post a Comment